Soaring Borrowing Costs Challenge the 2026 Spring Housing Market

New York, Tuesday, 24 March 2026.

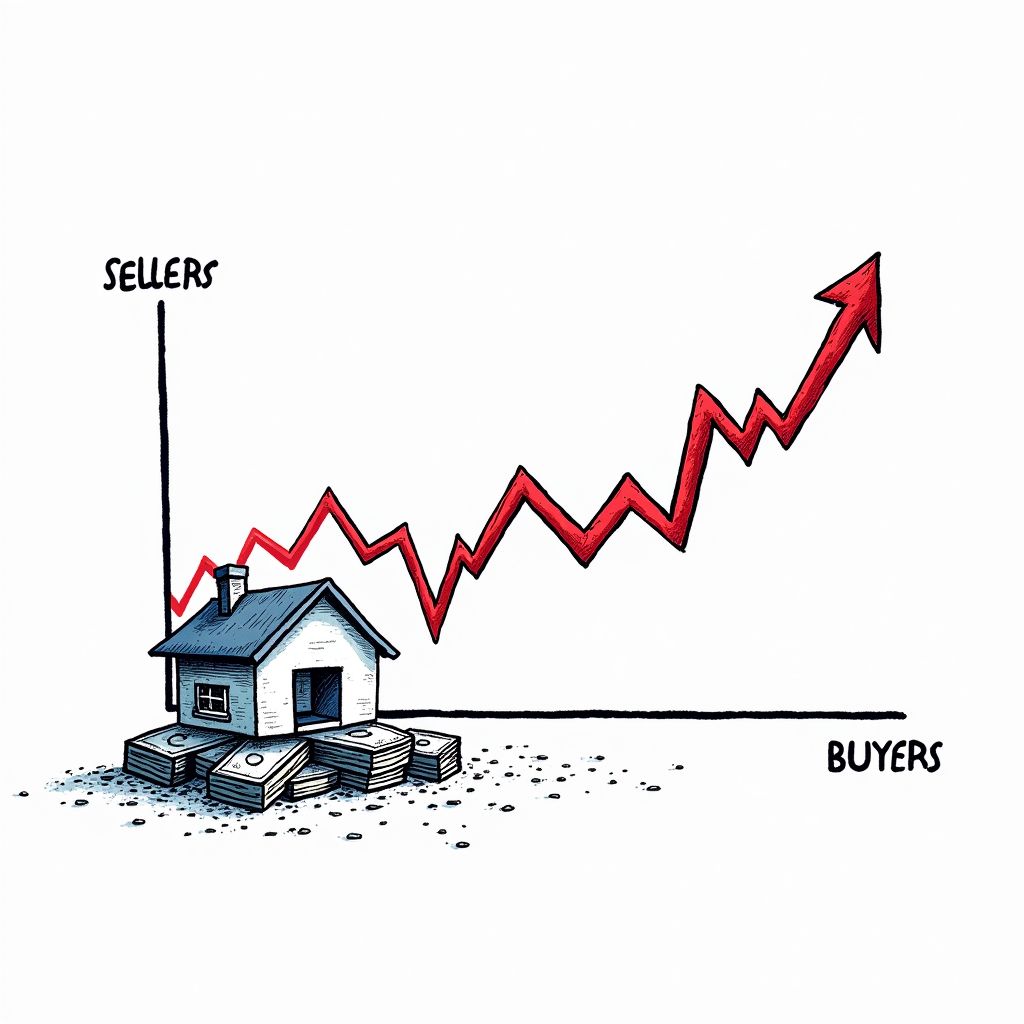

As March 2026 mortgage rates unexpectedly surge past 6.5%, the spring housing market faces severe headwinds, leaving a record-breaking 630,000 more sellers than buyers struggling to close deals.

The Macroeconomic Drivers Behind the Rate Spike

In early 2026, the average 30-year fixed-rate mortgage hovered around 6.21% to 6.22% [1][2][3]. However, by March 20, 2026, this rate sharply escalated to 6.53%, marking the highest level observed since September 2025 [2][4]. This sudden tightening in borrowing costs is primarily driven by rising oil prices and mounting inflation concerns, which have collectively pushed Treasury yields higher [2]. Furthermore, geopolitical tensions—specifically the ongoing war with Iran—have injected significant instability into global financial markets, directly influencing these elevated domestic mortgage rates [4]. Mortgage rates typically maintain a spread of approximately 2 percentage points above the 10-year Treasury yield, meaning any macroeconomic shock to bond markets immediately translates to higher costs for prospective homebuyers [2].

A Historic Imbalance: Buyers Retreat as Regional Disparities Widen

The spring 2026 housing market is defined by a staggering imbalance between supply and demand. In February 2026, the United States housing market recorded an estimated 1.99 million sellers compared to just 1.36 million buyers [5]. This translates to 46.3% more home sellers than buyers, creating a gap of approximately 630000 individuals—the largest such disparity recorded since 2013 [5]. The housing sector has technically been in a buyer’s market, defined as having over 10% more sellers than buyers, since May 2024 [5]. Despite this, active inventory for the week ending March 14, 2026, was up 5.6% year-over-year, yet new listings actually declined by 1.4% [4].

Construction Pressures and Legislative Responses

The new construction sector is also grappling with the dual pressures of high borrowing costs and shifting consumer demand. By January 2026, the inventory of new homes had swelled to a 9.7-month supply, while overall sales plummeted to their lowest levels since 2022 [4]. According to Bill Owens, chairman of the National Association of Home Builders, builders are confronting elevated land, labor, and construction costs [4]. To combat the affordability crisis and stimulate demand, nearly two-thirds of builders are now offering sales incentives and cutting prices as of March 2026 [2][4].

Navigating an Unsettled Economic Landscape

As the spring season progresses, the real estate market remains in a precarious position, caught between long-term improvements in affordability—driven largely by income growth—and sudden short-term macroeconomic instability [1][4]. The once-critical “lock-in” effect, which historically kept existing homeowners from selling due to favorable older mortgage rates, is finally beginning to ease, bringing more inventory to the market [1][5]. However, the anticipated return to a “normal” housing market, a balanced state unseen since 2018, remains elusive [1].